Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

By now you’ve heard that interest rates have hit over 7%, the real estate market has softened, and buyers and sellers are shifting their strategies in order to be successful. One of those emerging shifts includes a loan program known as the 2-1 Buydown. What exactly is a 2-1 Buydown and how does it work? Who benefits from a 2-1 Buydown? And is a 2-1 Buydown worth the hype? Let’s take a deeper look to answer those questions.

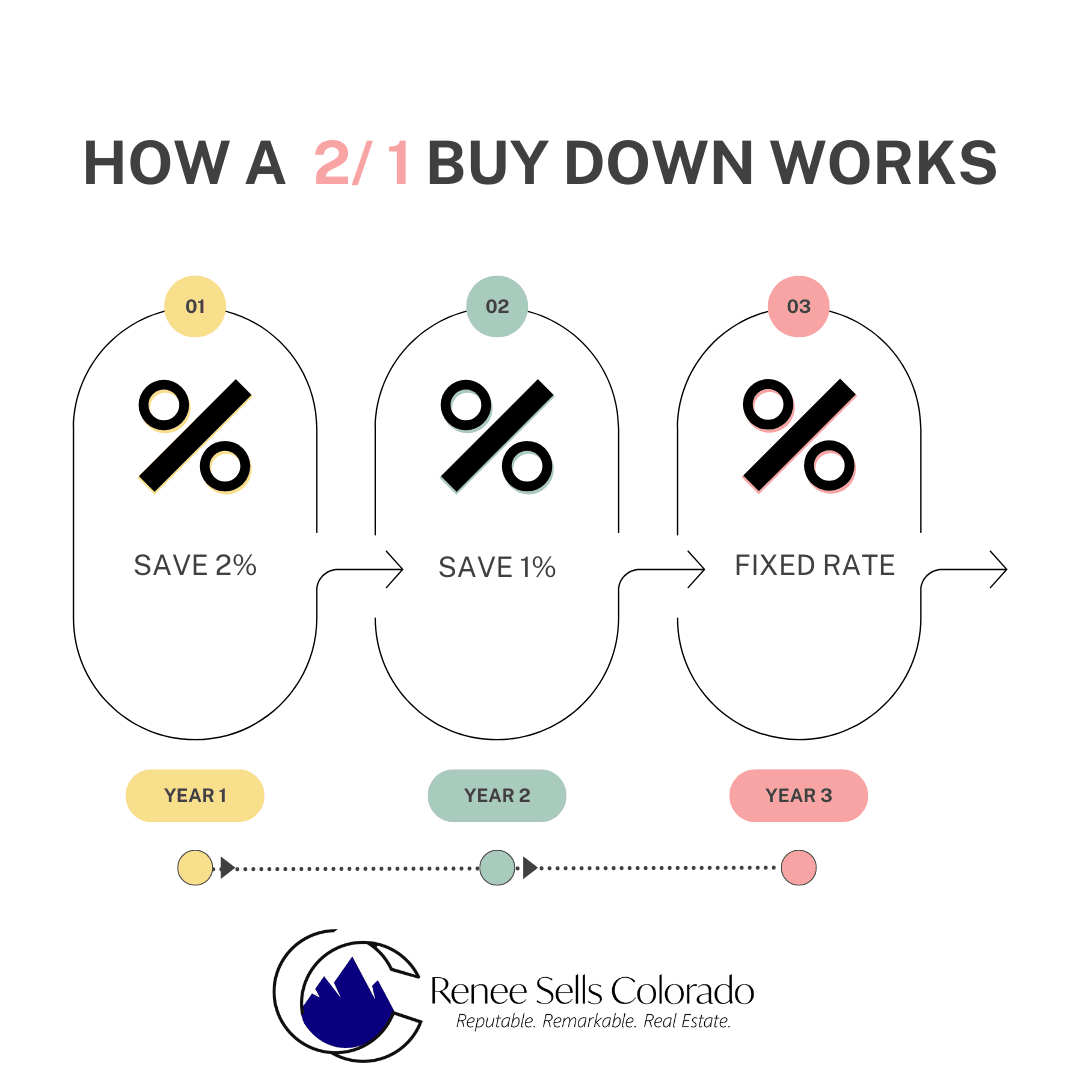

What is a 2-1 Buydown and how does it work?

Think back to when adjustable-rate mortgages were popular in the years immediately prior to the lending and housing crises in 2008. A 2-1 Buydown is essentially an adjustable-rate mortgage loan that allows the buyer to reduce their interest rate for the first two years of their loan. For example, a buyer with a 7% interest rate who opts for a 2-1 Buydown would pay 5% interest in Year 1 and 6% interest in Year 2, and then the interest rate would be fixed at 7% in Year 3 and beyond. Sounds great, right?

There is a twist, though – the Interest from Year 1 and Year 2 does not just disappear; that money is still paid during the first two years of the loan, and it must come from somewhere. The buyer can choose to pay it in a lump sum upfront as part of a loan cost, but in many cases, that money comes from the seller in the form of a concession given to the buyer at closing. For instance, a buyer with a 7% interest rate who was thinking of offering $680K on a $700K house instead offers a full price at $700K and asks for a $20K concession at closing. Rather than being given as a closing cost credit to the buyer, that $20K is deposited into an escrow account where those funds are drawn from monthly and used to make up the difference in the buyer’s monthly payment at 7% interest. So, for the first year, the buyer pays the principal and 5% interest and the remaining 2% interest is paid out of that escrow account, and in the second year the buyer pays the principal and 6% interest and the remaining 1% is paid out of that escrow account. Hmmm…interesting idea, right?

Who benefits from a 2-1 Buydown?

Both buyers and sellers can benefit from a 2-1 Buydown, although admittedly buyers are the ones who stand to gain more. The obvious benefit is a lower monthly mortgage payment for the first two years they own the home. However, this program resulted from our new climate of higher interest rates which directly impact a buyer’s buying power and affordability; therefore, buyers have to crunch the numbers and be mindful of the three different payment amounts for which they will be responsible all within a three-year time span, which is a short amount of time relative to both the life of a loan and annual salary increases.

The primary benefit for sellers is that their properties may remain affordable to a larger pool of buyers and they may be able to sell their homes faster than they would if their buyer pool shrank due to decreased buyer affordability. Buyers now have more choice in the market and more leverage in the negotiations, and sellers – after years of having to give up very little – have started to creatively incentivize buyers to choose their home over any others they are considering, and this loan program offers one such incentive. On the flip side, because the escrow funds often come from sellers, this now costs them money as their net proceeds from the sale will be lower. That leads us to answer the next question…

Is a 2-1 Buydown worth the hype?

The benefits are there, but there are risks too. Big ones. And that point cannot be underscored enough. First, buyers must truly understand how the program works to even consider this type of loan among their financing options. The underlying theory is that buyers’ incomes will likely increase, and they will become more financially stable as they accumulate increased equity and wealth, and therefore they will be in a better position to afford the higher payments when they go into effect a couple of years later. The theory goes one step further in thinking that buyers will in fact save the money not being spent now on mortgage interest; the question is just how many buyers will really do that, and the answer is likely not many.

Second, many buyers will focus only on the payments in the short-term, ie: Years One and Two, but they must consider the payments for the entire life of the loan; it’s imperative they qualify for and feel completely comfortable with the ultimate amount to which their payments will end up adjusting. If at the outset they cannot afford the payment at the increased amount, then the 2-1 Buydown is not a viable loan program for them.

Third, if enough buyers do not understand how the program works, this scenario has the potential to turn into a more pervasive disaster similar to the crisis from 15 years ago where buyers were foreclosed upon when their rates adjusted, and they couldn’t afford the payments. The Collective We learned a lot living through that crisis period and hopefully, we know enough to avoid another situation like that in the future.

In conclusion, the 2-1 Buydown is an intriguing mortgage option for buyers still trying to win in this market. Anyone opting for this loan program must fully understand how the program works and do their due diligence with number-crunching before signing on the dotted line. If the numbers work in your favor, this is a viable option; if the numbers are at all risky, seek other alternatives for your mortgage financing.